Mortgage Forbearance Fears

As part of the CARES Act (Coronavirus Aid, Relief, and Economic Security Act) recently signed into law by the President, forbearance has made the news in a big way. The CARES Act provides for some additional forbearance protections for homeowners that do not normally exist outside of the COVID-19 pandemic.

Under the CARES act, the servicer of any Federally backed mortgage is encouraged to waive all late fees, penalties and interest, and offer forbearance to any homeowners that request it.

What is unique about this guidance is that it may not even be necessary to prove that you are experiencing a financial hardship that would inevitably lead to the missing of mortgage payments in the future.

Unfortunately, this lower barrier to entry is being exploited and used as click-bait online without explaining ALL of the details about what forbearance means.

Our fear is that homeowners may knowingly or unknowingly take a mortgage forbearance without actually needing it, and without fully understanding the impact it can have on you and your family.

What is Mortgage Forbearance?

How can mortgage forbearance impact you? Well, the best way to answer this question is to first answer the question of what mortgage forbearance is.

Mortgage forbearance is a workout option for borrowers experiencing financial hardship. It allows you to not make your payments for a period of time, to be paid back at a later time.

Most forbearances being approved during the COVID-19 are 90 days minimum. 180 days of unpaid payments follow the guidance of the CARES Act, with an additional 180 days upon request.

While the duration of the forbearance period can vary depending on your situation, the forbearance solution is hardship workout by your mortgage servicer or lender allowing you to temporarily pay your mortgage at a lower payment or pause paying your mortgage.

If you’re unsure who your mortgage servicer is, the first place to start is to reference the contact information provided on your monthly mortgage statement.

Mortgage Forbearance Reinstatement

Once the forbearance period is up, you will have to pay the payment reduction or paused payments back. Paying back the skipped payments reinstates the original terms of the loan and you continue to make your payments as you did pre-hardship.

All forbearance programs require reinstatement in order for the loan to be in good standing, meaning you cannot refinance your loan while in forbearance. The expectation with a mortgage forbearance is that you will pay back the missed payments all at once.

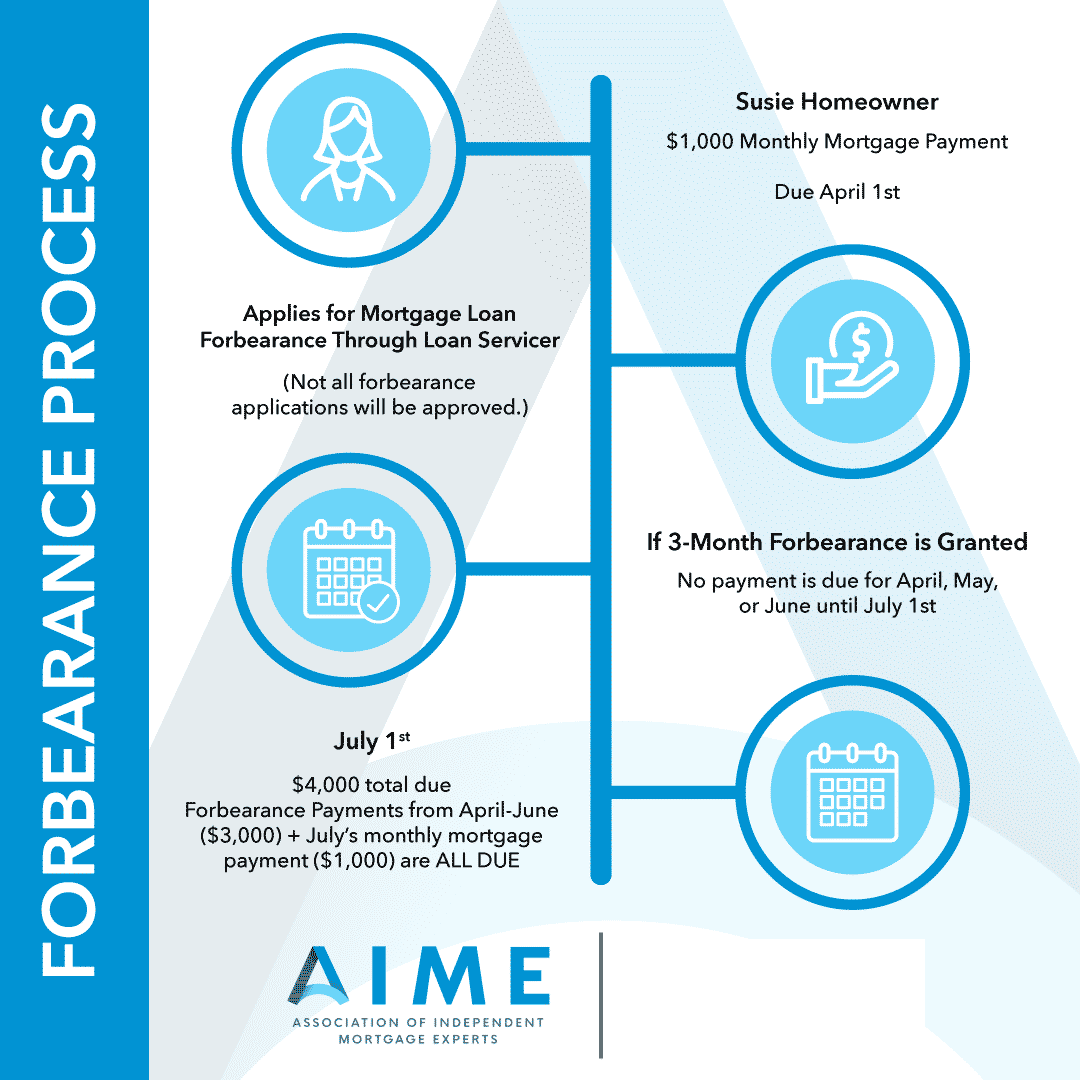

Pay Back Example – 90 Day Forbearance Reinstatement

This simple graphic created by the Association of Independent Mortgage Experts does a perfect job of walking you through a typical a 90-day forbearance example.

This is a very simple example, and it gives a good place to start when calculating what forbearance might mean to you. Now, for most folks that actually need forbearance to weather an unemployment period may not be in a position to come up with 3,6 or 12 months of missed payments all at once.

You’re most likely going to need another option for paying back missed payments.

More Options for Reinstating Your Loan After a Mortgage Forbearance

Options beyond paying back all missed payments at once vary from lender to lender (or servicer).

- Forbearance Extension – CARES Act recommends an initial 180-day forbearance with up to one 180 day extension.

- Paid Back Over Time – You may be able to pay back missed payments by adding to your regular payments until paid back.

- Payment Deferment – If Fannie Mae or Freddie Mac own your mortgage (click name to look up your loan), you may be able to move missed payments to the end of the loan term. This becomes a balloon payment that is due if you transfer title, refinance or sell your home in the future.

- Deed in Lieu of Foreclosure – If you are unable to qualify or unwilling to accept the workout option offered to you, a deed in lieu is an alternative to foreclosure that is also commonly known as “cash for keys”.

Experienced & Expert Advice

Any of the Vetted Professionals that you find thought this map or the private Facebook Group will be able to assist you in the Forbearance questions you may have.

Written by |